By Leen Shami

Making Housing More Accessible: How Rize Used Lean’s Open Banking Data to Cut Rejection Rates From 60% to 38%

In Saudi Arabia, most rental contracts require tenants to pay 6 to 12 months upfront, creating a significant barrier for individuals with stable income but limited cash on hand.

Rize is a leading Ejar-lease rental platform in KSA. The company pays landlords the full rent upfront, allowing tenants to repay their ejar payments in monthly installments instead of annual lump sums. This removes the upfront burden for tenants, expands access to housing, and ensures landlords receive their rent while filling units faster.

Challenges

Rize’s ability to scale depends on accurately identifying tenants who can afford monthly rent while maintaining strong underwriting standards. As demand for flexible rent payments grew, so did application volumes, reaching approximately thousands of applications per month.

However, this growth also exposed a key limitation in the way applicants were assessed.

Rize initially relied on traditional data sources to evaluate tenants. While these sources provide a useful baseline, they do not capture the full picture of an applicant’s financial standing. Income from bonuses, freelance work, transfers, or other non-traditional sources is often missing, leaving gaps in affordability assessments.

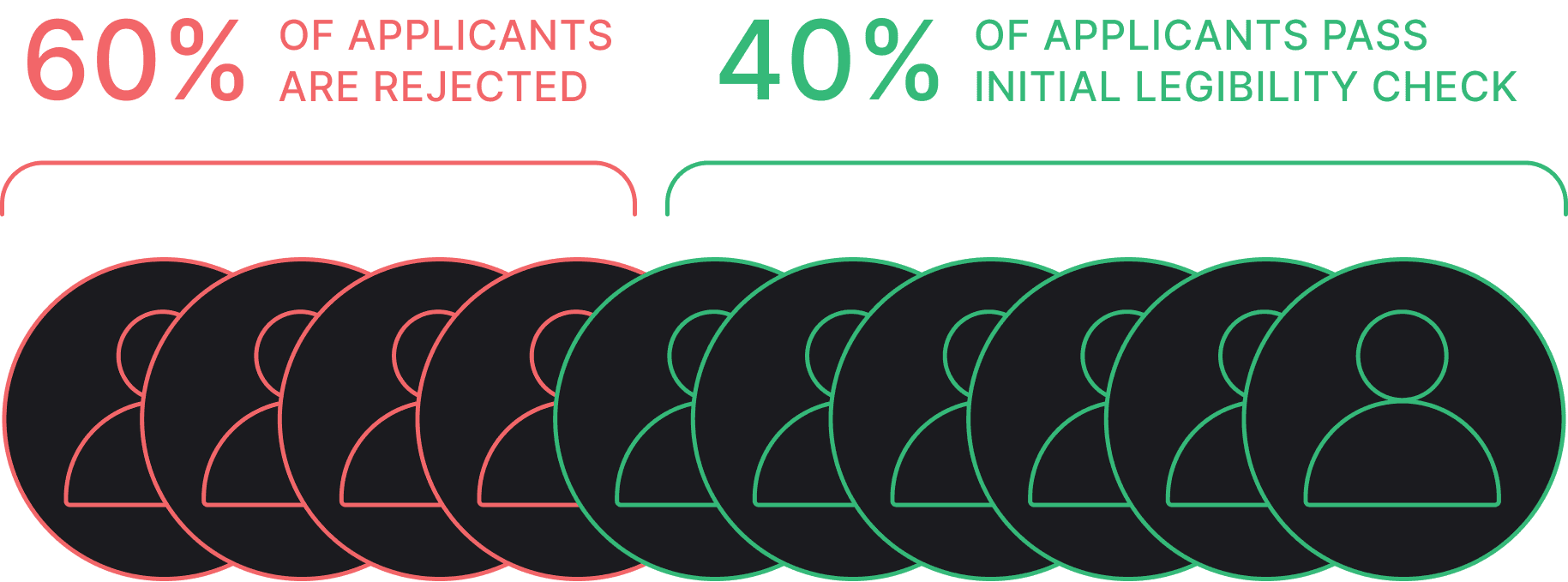

As a result, many financially capable tenants could not be approved with confidence. This became more pronounced at scale, with around 60% of applicants being rejected after initial checks from traditional data sources, despite some having sufficient income to afford monthly rent.

This gap had a direct impact on both sides of the marketplace:

- Applicants who could actually afford monthly payments were unable to access housing.

- As a result, landlords struggled to fill their units because applicants were not properly evaluated for their income.

Without a more accurate way to assess real income and affordability, Rize could not confidently convert this demand into approved tenants, limiting its ability to expand access to housing while maintaining risk controls.

Solution

Rize integrated Lean’s Open Banking Data to strengthen its underwriting process with verified, real-time income data.

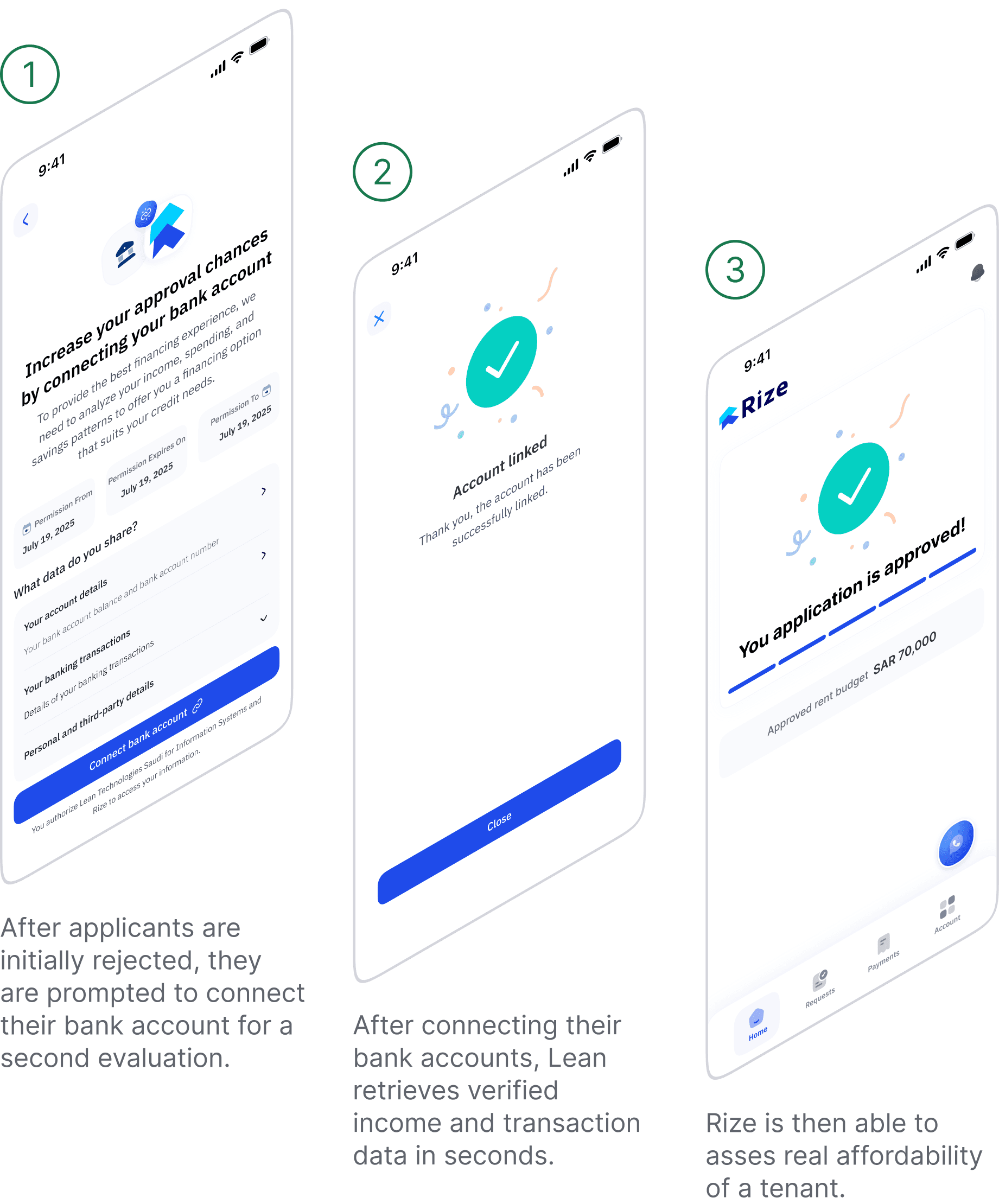

Applicants who are rejected are given the option to securely connect their bank account. This additional layer of visibility enables Rize to move beyond traditional data sources. Instead, applicants can be evaluated based on real income patterns, including salary, freelance earnings, bonuses, and recurring transfers.

This shift is particularly impactful for those who cannot be confidently approved using traditional data alone. Each month, approximately 15% of their applicants fall into this category, such as freelancers.

With Lean, Rize introduced a streamlined second-look flow:

- Applicants who cannot be approved based on traditional data are prompted to connect their bank account.

- Lean retrieves verified income and transaction data in seconds.

- Rize reassesses affordability based on real financial behavior.

This approach allows Rize to build a more complete and reliable view of each applicant’s ability to afford monthly rent, leading to faster decisions, reduced reliance on manual document checks, and more confident approvals at scale.

Results

By incorporating Lean’s Open Banking Data into its underwriting process, Rize approved more qualified applicants while maintaining strong risk controls.

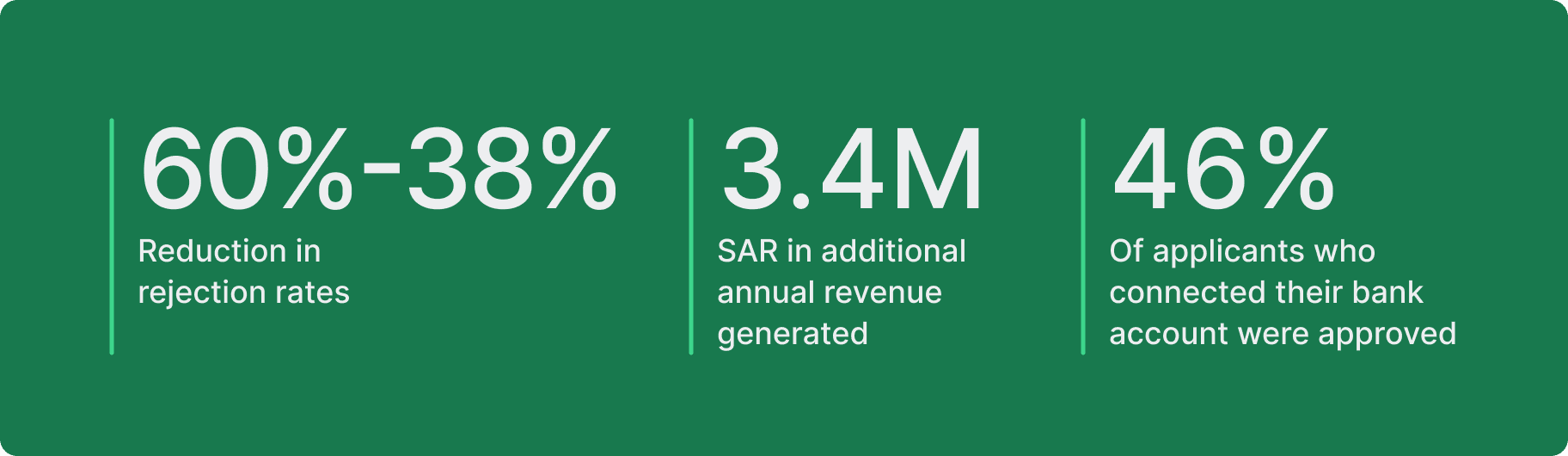

60% to 38% reduction in rejection rates

With a more accurate view of affordability, Rize significantly reduced its rejection rate from 60% to 38%. This enabled more financially capable applicants to access housing, accelerating approvals and reducing vacancy periods for landlords.

3.4M SAR in additional annual revenue generated

By approving applicants who would previously have been declined, Rize unlocked approximately 3,402,000 SAR in additional annual revenue. This reflects both an increase in approval volume and more efficient utilization of demand.

46% of applicants who connected their bank accounts were approved

Among applicants who connected their bank accounts via Lean, almost half were approved. This highlights that a meaningful portion of previously rejected applicants were financially qualified but could not be approved initially due to incomplete affordability assessments.

Continue reading

How Tamara Expanded Credit Access by 32% for the Modern Workforce with Financial Data

Tamara is Saudi Arabia’s homegrown FinTech platform, empowering millions of customers and thousands of merchants with innovative financial solutions. Founded in Riyadh, Tamara’s mission is clear: “We help people own their dreams”. Guided by this purpose, Tamara offers simple and flexible payments solutions, designed around how people manage their finances, inspiring greater control and confidence in their daily lives.

How Careem Pay Achieved 35% Lower Remittance Processing Costs

Careem Pay is the financial services arm of Careem, one of the region’s most recognized consumer digital platforms. With millions of users relying on Careem daily, Careem Pay is building financial products that make it easier to send and manage money across MENA through seamless P2P and international transfers, bill payments, and other digital wallet services.

How Open Banking can revamp customer onboarding and verification in the Savings Circles industry

Lean X Circlys | Case Study